by: Leonardo Corbucci 17 Luglio 2024 17:46

How an Industrial Photovoltaic System Works

To achieve the expected financial returns, it is important to monitor the photovoltaic system daily.

The photovoltaic sector has experienced significant development over the past three years, according to GAUDÌ data (see figure below).

In January 2020, the total installed capacity in Italy was 21,630 MW, while by the end of 2023, it exceeded 30,000 MW. This increase of approximately 9,000 MW is consistent with the decadal trend observed from 2011 to 2021.

Lately, there has been substantial discussion about photovoltaics, including the increase in installed capacity in MW, total production in GWh, and the nominal power of individual systems. However, there is considerably less dialogue about what it takes to establish a photovoltaic plant.

In this detailed exploration, we will examine every aspect, focusing on:

– The benefits and economic returns of investments.

– The importance of continuously and daily monitoring the systems.

Finally, we will provide guidance on the correct calculation of amortizations and the fiscal aspects mentioned in the current circulars from the Revenue Agency.

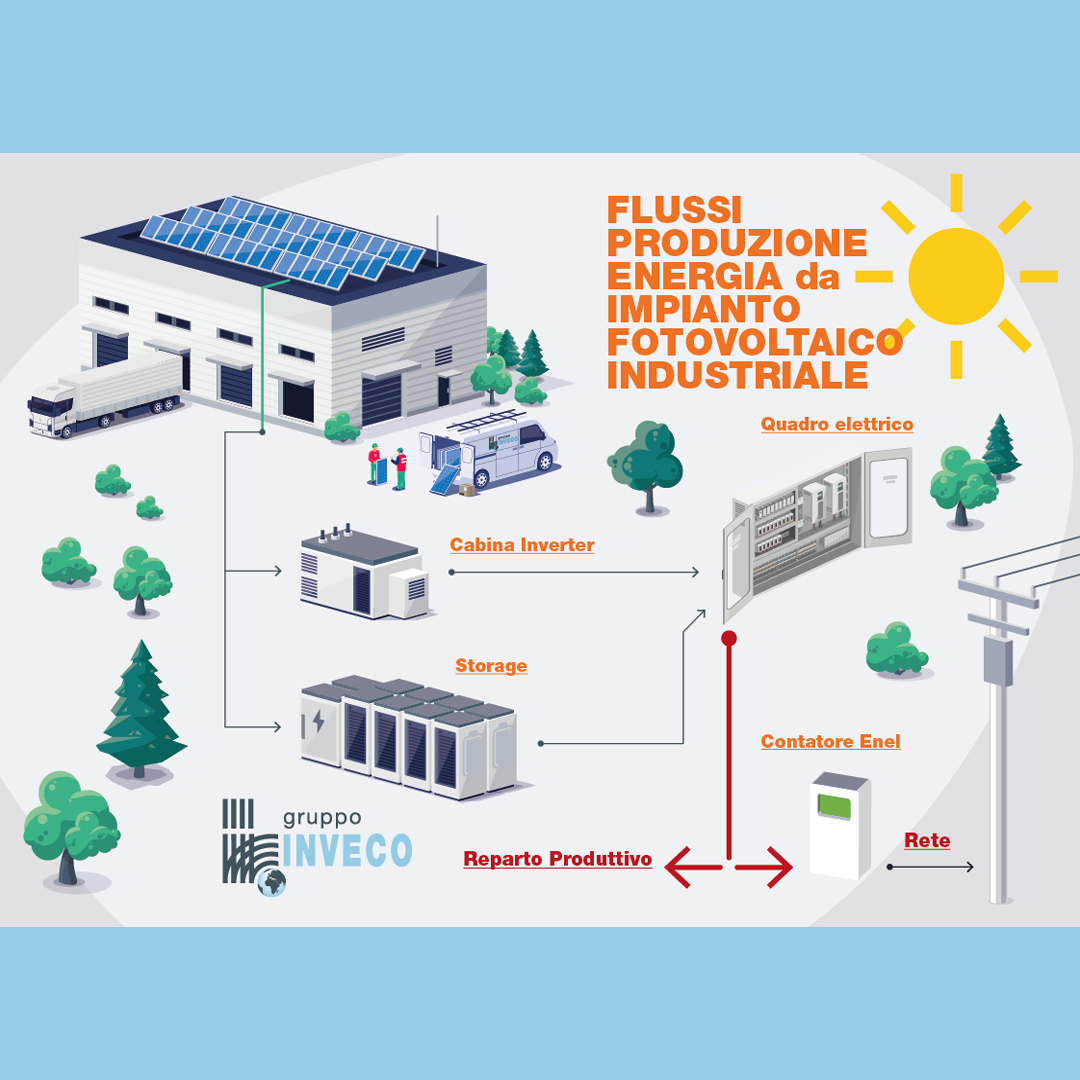

How a Photovoltaic System Works.

To understand the operation of an industrial photovoltaic (PV) system, it is essential to first comprehend its design and implementation.

We are discussing a typical Medium Voltage industrial PV system connected to the local electrical grid, operating in parallel with the network that powers the plant. The generated power supplements the electricity from the grid, thereby reducing the draw from industrial users.

The surplus energy, which occurs when the PV system’s output exceeds the plant’s consumption, is sold back to the grid.

To maximize the self-consumption of the energy generated by the PV system, a “Battery Storage” system is installed. This system is tasked with storing energy during the day, rather than exporting it to the grid, and then releasing it in the evening according to the plant’s needs, thereby optimizing self-consumption.

According to this rationale, photovoltaic technology is ideal for minimizing energy costs and achieving greater sustainability in industrial production.

The main components of a photovoltaic (PV) system.

Photovoltaic Modules: Panels composed of silicon cells (either polycrystalline or monocrystalline) that capture energy from sunlight.

The components of the module convert solar radiation into electrical energy (direct current). When connected in series, these modules form a string, and multiple strings connected in parallel constitute a solar generator.

Module Support Structures: These are the frameworks that hold the panels in place, attaching them to various types of industrial roofing.

Recently, to reduce the load on roofs, aluminum supports are being used.

Inverter: This electronic device converts the electrical energy produced by the modules (known as direct current) into the same type of energy used by industrial utilities (known as alternating current).

For increased safety, inverters incorporate protective devices that trigger shutdown in the event of a blackout or network disturbances.

Electrical Cables: The connection cables for photovoltaic panels that carry direct current are subjected to intense stresses. These are specific solar cables, equipped with good resistance to UV rays and weather conditions.

Protection Systems: These are the complex systems (e.g., switches, differential breakers, limiters, surge protectors) that safeguard the installation from adverse events such as overloads, short circuits, and lightning, or from direct contacts.

Measurement Systems: Photovoltaic installations connected to the grid feature a new meter installed by the local distributor, which measures production. This meter complements the existing one in the facility, thus measuring the exchange of produced energy with consumed energy and any energy fed into the grid: these are called “bi-directional meters”.

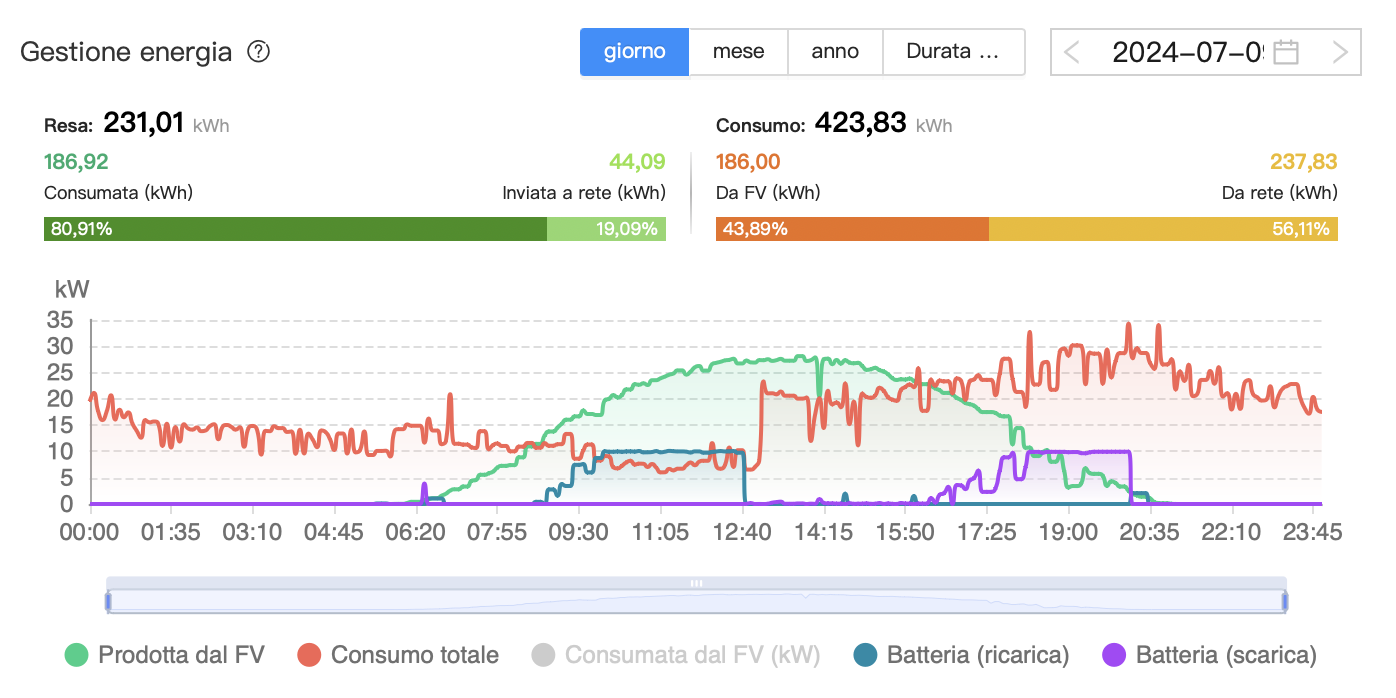

Monitoring System: This is a system that allows remote control of one’s installation, monitors production performance and self-consumption, and checks the status of inverters.

Data related to the plant’s production in kWh are transferred to a “smart logger” which, connected to a customized service server by the monitoring system manufacturer, displays various functions to the user. At the management level, various specific settings can be made, and at the reporting level, it is possible to interpolate production, consumption, discharges, and charges of the storage, and so forth.

Legend:

> The orange line indicates the consumption of the industrial facility;

> The green Gaussian represents the energy production generated by the photovoltaic system;

> The cobalt curve denotes the temporary interval during which the storage system is charged daily;

> The purple curve indicates the temporary interval during which the storage system operates in parallel with the photovoltaic production to reduce the facility’s consumption.

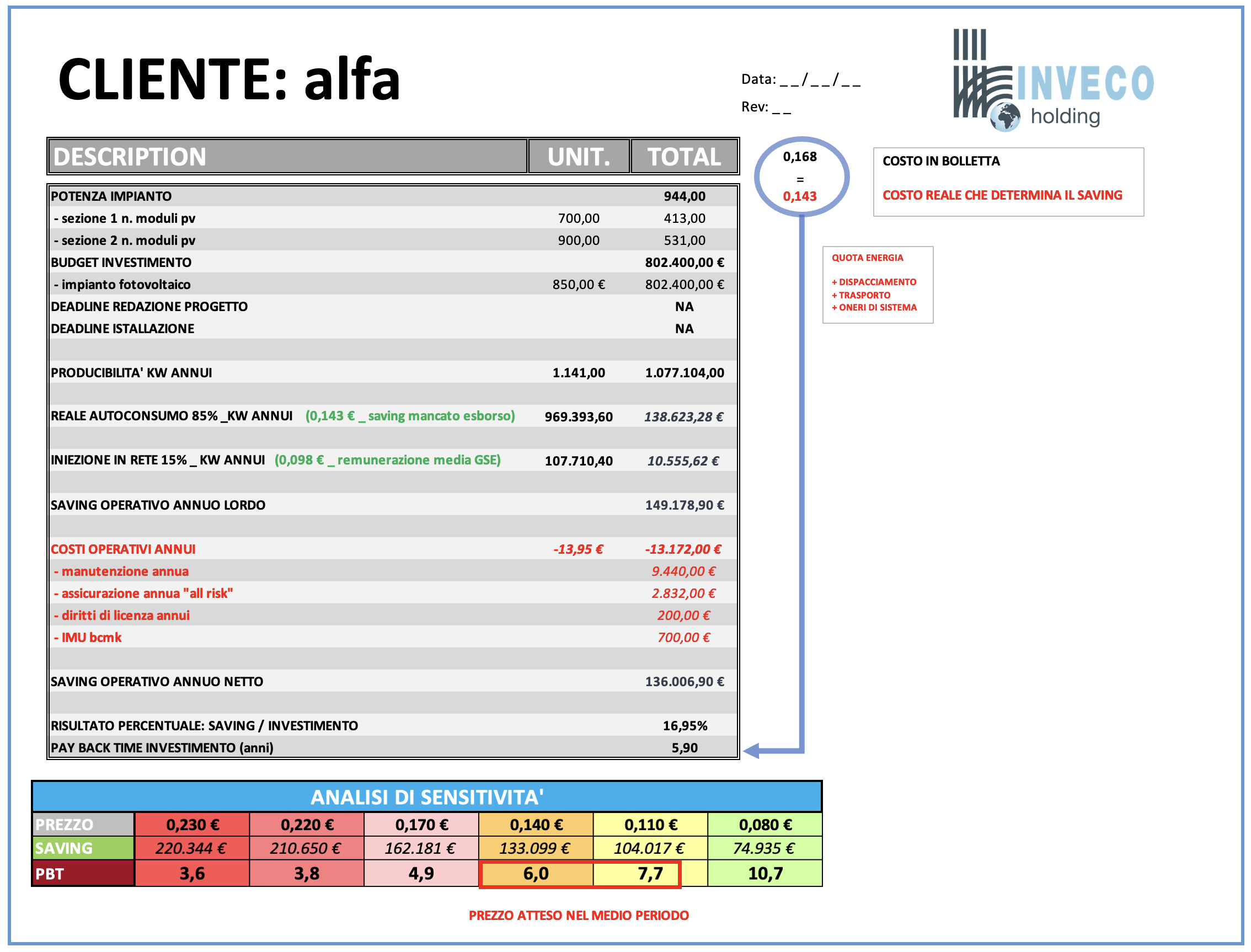

Economic Benefits and Return on Investment of a Photovoltaic System.

To understand the economic benefits and return on investment of a photovoltaic system, it is necessary to evaluate the average annual savings from the reduced need for electric energy payments, combined with the revenues from grid feed-in.

Let’s consider a very practical example:

“Given the cost of investing in a 944 kW industrial photovoltaic system, with an expected average annual output of 969,393 kWh (1,141 kWh/kWp – central/northern Italy geographic area), of which 85% will be directly consumed by the industrial facility’s utilities and the remaining 15% will be ‘Grid Connected’, we would see the following economic benefits:

– A GROSS ANNUAL OPERATIONAL SAVING of €149,006, from which ANNUAL OPERATIONAL COSTS are deducted, resulting in a NET ANNUAL OPERATIONAL SAVING of €136,006.

– When related to the initial investment, this results in a PAYBACK PERIOD of 5 years and 9 months.

If we consider that the cost of electricity varies over time, through sensitivity analysis we can identify the variability of the investment return over periods that fluctuate by a few months from one case to another.”

To ensure the economic benefits outlined, it is essential to consider periodic maintenance of the system and daily monitoring as instrumental.

Monitoring a system is crucial because it allows you to remotely assess real-time production and thus promptly intervene in the event of faults and system anomalies.

Calculation of the Depreciation of a Photovoltaic System.

Article 23, paragraph 47, of the decree dated July 6, 2011, no. 98, had established that, starting from 2013, the rules governing the tax depreciation of tangible assets would be revised.

This update was set to be very significant for the renewable energy plant sector, as the new technologies employed in these projects would finally receive specific depreciation rates.

Indeed, this regulation was adopted at the end of 2013. However, there was a shift in interpretation by the Italian Revenue Agency, which turned out to be less favorable regarding the applicable depreciation rate for photovoltaic systems.

Initially, in 2007, the Revenue Agency had considered the depreciation rate for these assets to be 9%, classifying them as movable goods (circular dated July 19, 2007, no. 46/E).

Contradicting its earlier stance, in 2013, the Revenue Agency changed its approach. It deemed larger photovoltaic systems to be of a real estate nature and determined that in such cases, the applicable depreciation rate should be 4%, as specified for “buildings used for industrial purposes” (circular dated December 19, 2013, no. 36).

For movable goods, the Revenue Agency applied the depreciation rates intended for thermoelectric power production plants (Group XVII, type 1/b), which is 9%.

However, concerning real estate, since the decree specified that buildings are excluded from this definition, a different depreciation rate of 4% is considered applicable.

Therefore, and as a result of this approach, the Tax Administration, in the same circular no. 36/2013, expressed its stance on the depreciation rate for photovoltaic systems, effectively linking it to whether the system is classified as real estate or personal property for tax purposes.

The fiscal entity fundamentally considers applicable:

– A depreciation rate of 9% exclusively for photovoltaic systems that can be classified as movable goods, akin to thermal power plants;

– A depreciation rate of 4% for buildings used for industrial purposes, applied to photovoltaic systems that can be classified as real estate.

This stance taken by the fiscal entity, which has led to significant criticism and numerous tax disputes, has been the subject of a specific publication by the Italian Association of Chartered Accountants (Behavioral Norm No. 197 of July 18, 2016). This document preliminarily delves into the accounting treatment prescribed by the national accounting principle (OIC 16).

From an accounting perspective, as described by OIC 16, the value of a complex energy production plant (from photovoltaic, wind, or thermal sources) must be broken down based on the nature of its components, according to the categories of tangible fixed assets identified by Article 2424 of the Civil Code.

Furthermore, if an economic-technical unit is identified—meaning a set of assets coordinated in a technical-production logic—it is necessary to determine the values of the individual assets that comprise it, distinguishing between those subject to depreciation (further divided based on their useful life) and those that are not.

OIC 16 also specifies that depreciation of components, fixtures, or accessories (included in a complex asset) characterized by different useful lives must be calculated separately for each (referred to as the “component approach”).

Therefore, already at the stage of recording the value in the financial statements, the value of the complex structure of the electrical energy production plants must be decomposed by components according to nature, depreciable status, and useful life, based on market prices and taking into account the condition of the assets.

The publication continues by analyzing the subsequent tax profile related to the correct depreciation of these assets, introducing some reflections that effectively “surpass” the approach of the Revenue Agency.

Here is the professional English translation of the text provided:

The Italian Association of Chartered Accountants notes that:

> The purpose of the ministerial decree is to categorize tangible fixed assets by their nature in order to determine their useful life, expressed in terms of differentiated depreciation rates;

> The classification of photovoltaic systems as buildings (by analogy to thermal power plants) proves useful in instances where the assets are not easily distinguishable from one another (i.e., tangible assets of different natures with different useful lives that are assembled to perform a complex function);

> Unlike thermal plants, photovoltaic (and wind) installations are mostly exposed to weather elements, being housed within smaller buildings only optionally and to a marginal extent (e.g., electrical substations and cabins).

It concludes that:

> For building components, which have a longer period of depreciation, a 4% depreciation rate would be applicable;

> For the plant components (fundamental elements) of photovoltaic installations, whose identification derives from the analysis of how they perform their essential function, represented by the production of electric power, a 9% depreciation rate would instead be applicable;

> Different depreciation rates provided in the decree dated December 31, 1988 (at Group XVII, species 1/b) would apply to components separately listed.

The only exception would be the support structures for the panels, which due to their nature as constructions and their durability, can be assimilated to buildings, even from an accounting and fiscal perspective.

Finally, it is highlighted that this approach, developed by the Order of Chartered Accountants (and absolutely agreeable from both a legal and technical perspective), was the subject of specific parliamentary inquiry no. 5-09541 on September 22, 2016, to which the Minister of Economy and Finance responded negatively.

In essence, the government has reiterated the position expressed by the Revenue Agency (circular 36/E of December 19, 2013), namely the depreciation rate of 9% (on assets qualified as movable) and 4% (on those qualified as immovable).

The response to the inquiry thus leaves open the issue of the divergence between civil and tax regulations (which must be subject to individual and specific assessment by the entrepreneur and the accountant), inevitably resulting in a continuous increase in tax litigation.

Conclusion

In conclusion, the development of a photovoltaic system requires not only technical expertise but also meticulous management of economic and fiscal components. With continuous monitoring, it is possible to ensure a secure and sustainable return on investment, while simultaneously reducing energy costs and protecting the environment.

Recent Posts

Categories